For Ryan Porter, a 25-year technology veteran currently working with AWS, real estate investment has grown from an opportunistic side project into a calculated cross-border operation. As a P...

Distressed Office Assets Draw Contrarian Investor Despite Market Headwinds

Written by:

Date:

14 Jan 2026

Share via Facebook

Share via Linkedin

Share via X

Copy to clipboard

As most commercial real estate investors pull back from the office sector, a small group of experienced operators is actively seeking opportunities in distressed office assets. Elevated vacancy rates, persistent concerns about the impact of remote work, and ongoing urban challenges have pushed many investors to the sidelines. Yet for some, these pressures have created entry points for long-term strategies focused on repositioning and adaptive reuse.

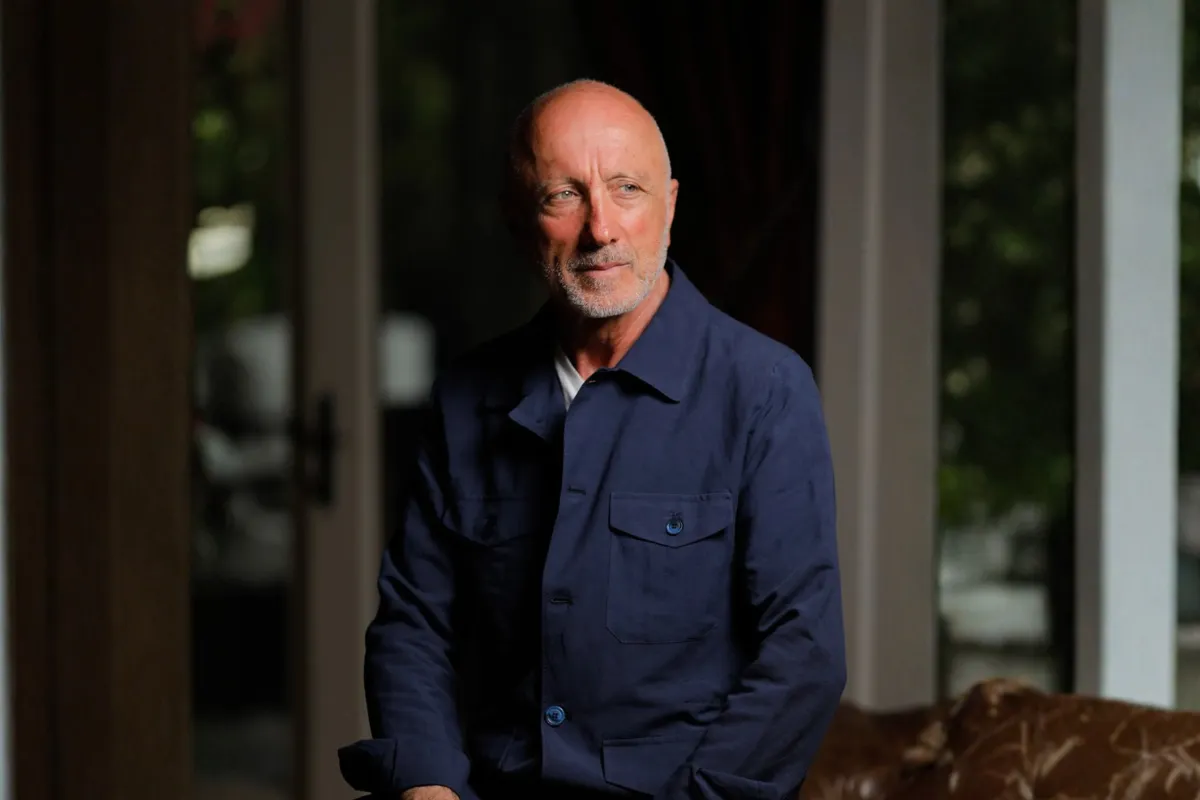

Izek Shomof, founder and CEO of Shomof Group, is among the few investors aggressively acquiring office properties in Los Angeles at steep discounts to pre-pandemic valuations. Shomof’s approach is a calculated bet that the current distress offers value for those willing to invest in substantial improvements and pursue multiple exit options.

“I’m seeing properties that, in their good days up until two years ago, were selling for four hundred million dollars, and today, due to the vacancy, the price has dropped significantly. Now I’m buying them at fifty cents on the dollar,” Shomof says. “That’s where I see the opportunity, and I’ve done that twenty to thirty years ago and succeeded.”

Urban Challenges Continue to Weigh on Office Values

Los Angeles faces the same urban challenges as many major U.S. cities. Persistent issues with public safety and homelessness, along with a slow return to urban offices, have weighed on both property values and tenant demand. While Shomof notes that conditions have shown marginal improvement over the past year, he emphasizes that these challenges are still a significant factor in the current market.

“There are still challenges here in downtown LA. It’s improving since the last time, but it can improve much better,” he says, highlighting how these issues directly impact occupancy rates and tenant comfort.

For investors like Shomof, these urban problems are both sources of risk and opportunities. The resulting distressed pricing creates potential for outsized returns, but only for those willing to address the factors that have driven values down in the first place. This requires a proactive management approach, including tenant engagement, security upgrades, and community improvements.

Location as the Cornerstone of Office Investment

Despite broad skepticism about the future of office real estate, Shomof argues that demand for well-located properties remains strong. His investment thesis centers on the belief that quality office space in prime areas will continue to attract tenants, even if overall demand remains lower than in the past.

“There are still people who want to rent offices. Not as much as it used to be back in its good days, but there are still people who want to rent offices,” he says. “If it’s in a good location, I do believe that people will come back to offices.”

Rather than simply buying and holding distressed assets, Shomof’s strategy involves comprehensive neighborhood improvement. “We go to a distressed area, and we improve the area. We fix the street, we create retail, we bring up the building, put more security, making it more appealing, and make the tenants feel comfortable and safe,” he explains.

This focus on active management and area revitalization is designed to differentiate Shomof’s assets in a competitive leasing environment and improve long-term occupancy rates.

Conversion Flexibility: Built-In Risk Mitigation

A central component of Shomof’s approach is maintaining flexibility through multiple exit strategies, especially the potential for office-to-residential conversions. Rather than relying solely on an office market rebound, he seeks properties that can be repositioned into residential use if necessary—a strategy he has used successfully in past downturns.

“If offices will completely die out, which I doubt that they will, I’m looking for other alternatives. If I can take that property and convert it into residential, and if it’s doable to convert them into residential, that is my other alternative,” Shomof says.

This dual-path approach provides downside protection and the ability to capitalize on whichever market—office or residential—proves stronger. The conversion option has become increasingly relevant as urban areas continue to experience strong housing demand, even as office demand remains uncertain.

Shomof’s experience with adaptive reuse spans decades. “I have done it in the past. I’ve done it twenty to twenty-five years ago with adaptive reuse, and I believe I can do the same this time around if needed,” he says.

Thorough Due Diligence and Risk Assessment

Shomof emphasizes that success in acquiring distressed office assets depends on rigorous due diligence and a clear understanding of all viable repositioning options before committing capital.

“It’s always before you buy it to create options,” he says. “I wouldn’t buy it without options. It’s always ‘what if that doesn’t work? What will I be able to convert it into?’ Residential will always be occupied.”

Lessons from previous market cycles shape this disciplined approach to risk management. It enables investors to avoid overexposure to a single outcome and ensures that each asset has at least one viable alternative use if office recovery fails to materialize.

Market Timing and Long-Term Perspective

The current market is defined by uncertainty and caution, with many investors waiting for more evident signs of recovery before reentering the office sector. Rising interest rates, tighter lending standards, and a more cautious approach from institutional buyers have all contributed to a slower pace of transactions.

Shomof acknowledges these headwinds but maintains an optimistic long-term outlook. He believes that market distress offers unique opportunities for those with patient capital and the willingness to engage in active management.

“They always say that it’s going to get worse before it gets better. Could be. I’m an optimist, and I’m hoping for the best,” he says.

This outlook is not based on wishful thinking, but on a strategy that combines discounted acquisitions, flexible repositioning options, and hands-on operational improvements. For Shomof, the current downturn is a repeat of earlier cycles where distressed buying and active management produced strong returns for those who acted while others hesitated.

Key Takeaways for Investors Considering Distressed Office Assets

Shomof’s approach offers several clear lessons for commercial real estate investors evaluating distressed office properties in today’s market:

- Location remains critical: Even in a challenging environment, well-located assets are more likely to retain tenant demand and offer multiple repositioning options.

- Multiple exit strategies are essential: Investors should prioritize assets that can be converted to alternative uses, such as residential, if office demand fails to recover.

- Active management drives value: Successful repositioning requires more than capital—it demands a hands-on approach to area improvement, tenant engagement, and building upgrades.

- Thorough due diligence is non-negotiable: Understanding all potential outcomes and creating options before acquisition is crucial to managing risk.

- Patience and expertise are rewarded: The current environment favors investors with long-term capital, operational experience, and the ability to navigate complex repositioning projects.

For those with the resources and expertise to execute comprehensive repositioning strategies, the combination of significant discounts to replacement cost, flexible exit options, and active management may offer a rare window to achieve attractive returns. As mainstream capital remains cautious, contrarian investors like Shomof are capitalizing on opportunities that emerge only during periods of market distress.

The next phase for the office sector remains uncertain. However, the actions of experienced operators suggest there is still an opportunity for those prepared to address the sector’s current challenges head-on. For now, the distressed office market belongs not to the cautious, but to the contrarians willing to engage, improve, and adapt.

Similar Articles

Explore similar articles from Our Team of Experts.